9 Budgeting Methods to Consider

Here are nine budgeting strategies to help you find what works best for your mindset, income, and lifestyle.

1. Zero-Based Budgeting

Every dollar has a job. With zero-based budgeting, your income minus your expenses (including savings and debt payments) should equal zero.

Best for: People who want a high level of detail and control over their finances.

Pros: Helps identify waste, encourages intentional spending.

Consider: It requires consistent tracking and discipline.

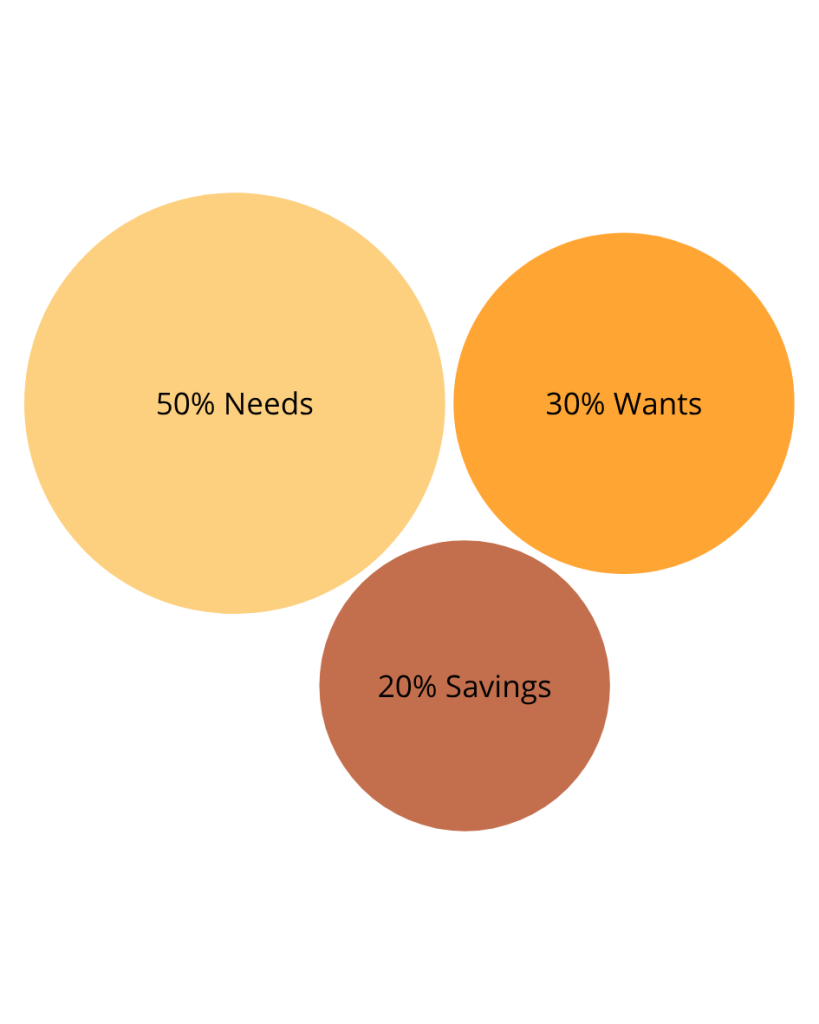

2. The 50/30/20 Rule

This method divides your income into:

-

- 50% for needs

- 30% for wants

- 20% for savings and debt payments

Best for: Folks who want a balanced, straightforward framework.

Pros: Easy to follow and adjust.

Consider: May not be realistic in high-cost-of-living areas or for those with irregular income.

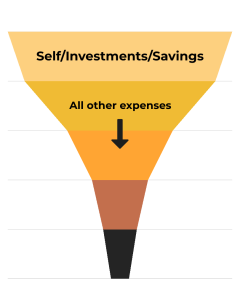

3. Pay Yourself First

You prioritize savings and investments first – before spending on anything else.

Best for: People focused on building savings, retirement, or wealth goals.

Pros: Automates good habits and builds long-term security.

Consider: Requires strong awareness of what remains for daily expenses.

4. Envelope (or Digital Envelope) System

You divide your spending into categories and assign a set amount to each (traditionally with physical envelopes) but apps can do this digitally now.

Best for: People who tend to overspend and need clear boundaries.

Pros: Visual, easy to understand, great for variable spending.

Consider: Can be time-consuming to set up and maintain manually.

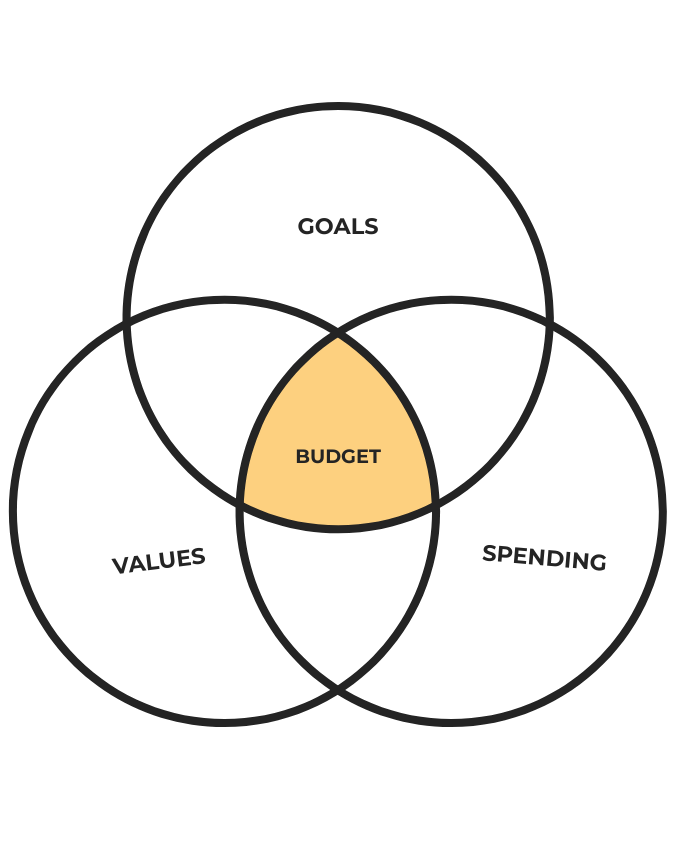

5. Values-Based Budgeting

This method starts with your core values. You direct your money toward what brings meaning, joy, or alignment in your life.

Best for: Those who want their money to reflect their personal or social values.

Pros: Helps reduce guilt, enhances motivation.

Consider: Requires self-reflection and may not always align with traditional “shoulds.”

6. Anti-Budget

This approach flips the traditional budget on its head. You decide how much you want to save and invest each month, then spend the rest however you want.

Best for: Minimalists and those who hate tracking every dollar.

Pros: Low maintenance, highly flexible.

Consider: Only works if you’re disciplined with saving first.

7. Percentage-Based Budgeting

Instead of assigning dollar amounts, you assign spending categories a percentage of your income.

Best for: People with fluctuating income or commission-based work.

Pros: Scales with your income.

Consider: Requires adjusting allocations monthly based on earnings.

8. Calendar-Based Budgeting

You plan your expenses around when bills are due and income is received, mapping out your month like a calendar.

Best for: Those who live paycheck-to-paycheck or have variable income.

Pros: Helps with cash flow timing and avoids overdrafts.

Consider: Can be time consuming to track everything by date.

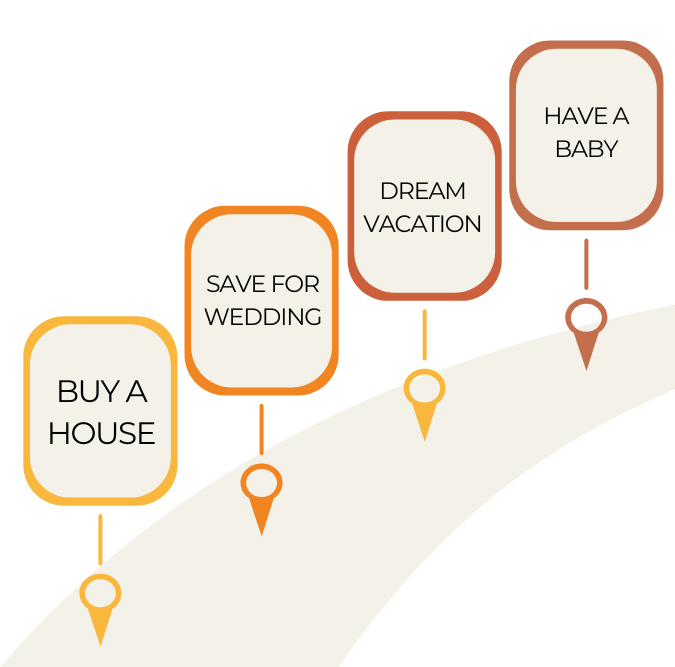

9. Goal-Based Budgeting

You focus your budget around specific short or long term financial goals, like paying off a credit card, saving for a vacation, or buying a house.

Best for: Motivated planners and visual thinkers.

Pros: Builds momentum and focus.

Consider: May overlook day-to-day spending habits if not balanced.

Budgeting Methods for Variable Income

If your income changes from month to month, finding budgeting methods for variable income that actually work can feel extra challenging, especially for entrepreneurs, freelancers, and creatives.

But it’s absolutely possible.

Tips on budgeting for variable income:

-

- Start with your bare minimum expenses. Know the least amount you need each month to cover essentials.

- Build a buffer. Save during high-income months to carry you through the leaner ones.

- Use percentage-based or pay-yourself-first methods. These scale better with changing income.

- Prioritize flexibility. Your budget should be adaptable month-to-month.

A variable income doesn’t mean you can’t plan, it means your plan needs to move with you.

Find Your Fit, Not a Formula

Budgeting isn’t one-size-fits-all. Your income, your habits, your goals – they’re all uniquely yours. Start by experimenting. Mix methods. Adjust monthly. Make it fit your life.

At Citrine & Gold we like to follow the method, “Track, Assess, and Adjust.”

Ready to get started?

Download our free budget spreadsheet and check out our financial planning services to take your budget to the next level.